Commercial real estate (CRE) has been a source of concern for the economy and financial system over the past year, but there have been some recent signs of the sector steadying itself amid lingering challenges. Despite depressed activity, the CRE industry has been resilient and projects could pick up when general economic conditions improve. Banks will be an important component in providing capital for CRE companies as they pursue new development as conditions improve. CRE customers who bring a balanced revenue profile will be most supported by banks.

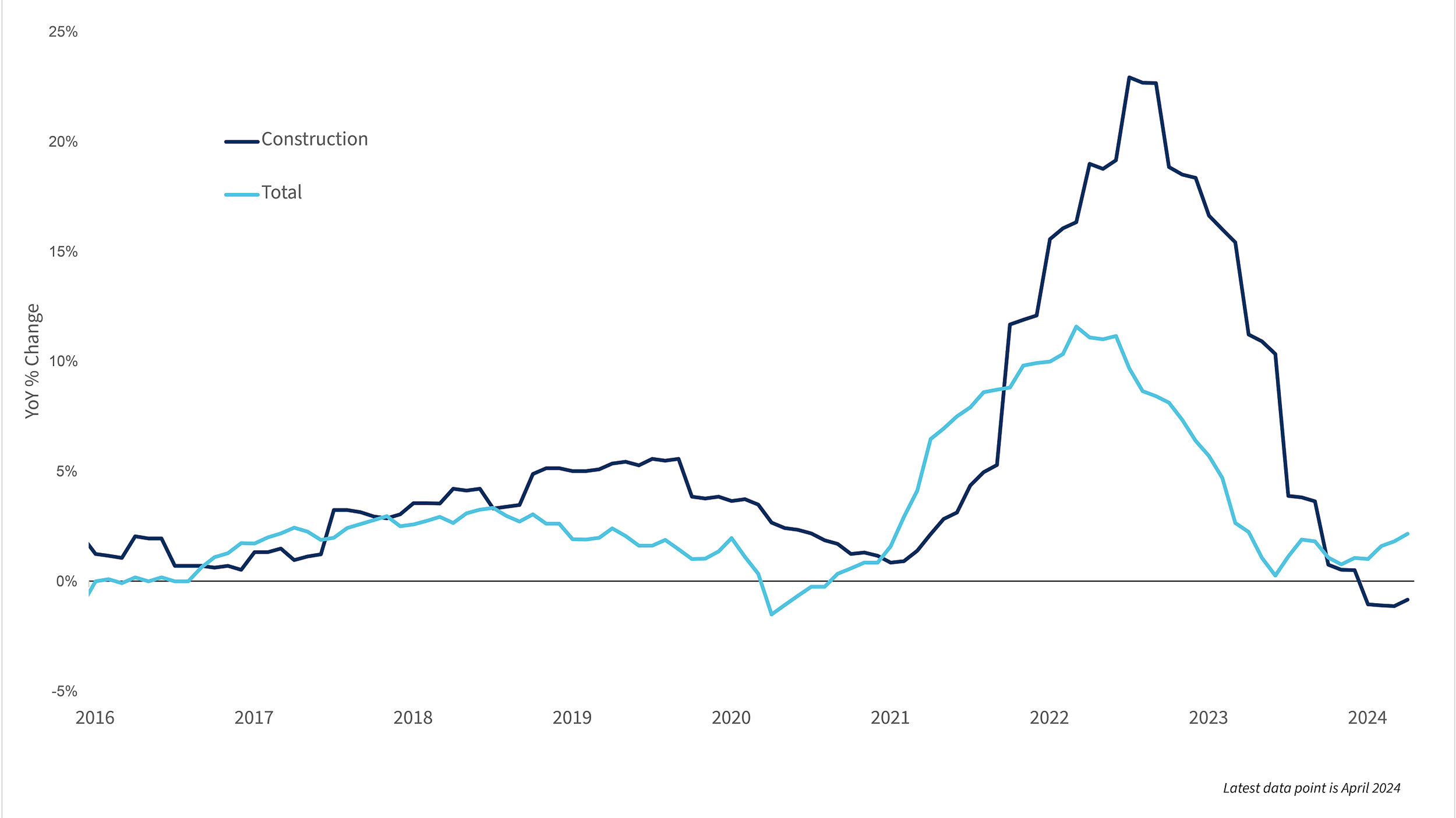

One factor that is putting pressure on commercial real estate developers and operators is the rising cost of doing business. High construction and operating costs combined with flat rents are making conditions difficult. Construction costs have increased at an elevated rate in Minneapolis, rising 37% since 2019 (compared with just 12% between 2014 and 2019). Nationwide trends are similar, with construction costs up 36% since 2019. These conditions displayed signs of modest improvement in the recent Minneapolis Fed Construction Sector Outlook Survey, though revenue and profits remain net-negative. On the bright side, the survey also showed that labor demand is solid and labor availability is improving.

Another factor contributing to high operating expenses is the dramatic rise in insurance costs over the past year. The increasing prevalence of extreme weather events as well as the rising costs of litigation have made insurance more expensive.

In 2023, there were 28 weather and climate events which caused at least $1 billion in insured and non-insured losses nationwide, compared to the previous annual record of just 22, according to the Insurance Information Institute. This dramatic increase drove property and casualty insurance inflation despite a slowdown in price increases in many other areas. Inflation for property and casualty insurance, as measured by the producer price index (PPI), has increased 7% over the past 12 months, in contrast to broader PPI inflation which cooled to just 2.2% over the past year.

PPI inflation1

High interest rates, labor market shortages and persistent inflation have had varied impacts across different CRE sectors. Office CRE activity remains depressed as many employees continue to work remotely, keeping vacancy rates high. Over a third of employees in Minnesota work remotely some or all of the time, according to the Federal Reserve Bank of Minneapolis. Though there has been lots of conversation about converting office space to apartment buildings, in reality, this process is costly and complex. Office space returns are down 14.7% on a year-over-year basis in the Midwest, according to the NCREIF Property Index (NPI), due to slow activity and ongoing pessimism.

Unlike office activity, industrial and manufacturing construction did surge due to pandemic-related supply chain difficulties and onshoring prioritization. However, absorption in this area is showing signs of slowing down with the industrial NPI declining 5.5% year-over-year in the Midwest.

The NCREIF retail index is down 3.79% year-over-year in the Midwest but remains stronger than many other sectors. Because retail properties are typically financed with longer-term, fixed-rate loans, the sector has remained more insulated from interest rate volatility. Strong consumer spending and limited new retail construction have also contributed to the sector performing relatively well.

The hospitality and senior housing sectors of CRE have also made strong comebacks with top line revenue at an all-time high. However, as noted earlier, operating costs remain elevated and labor market challenges are having a particular impact on these sectors.

Interest rates2

Financial partners can help with road ahead

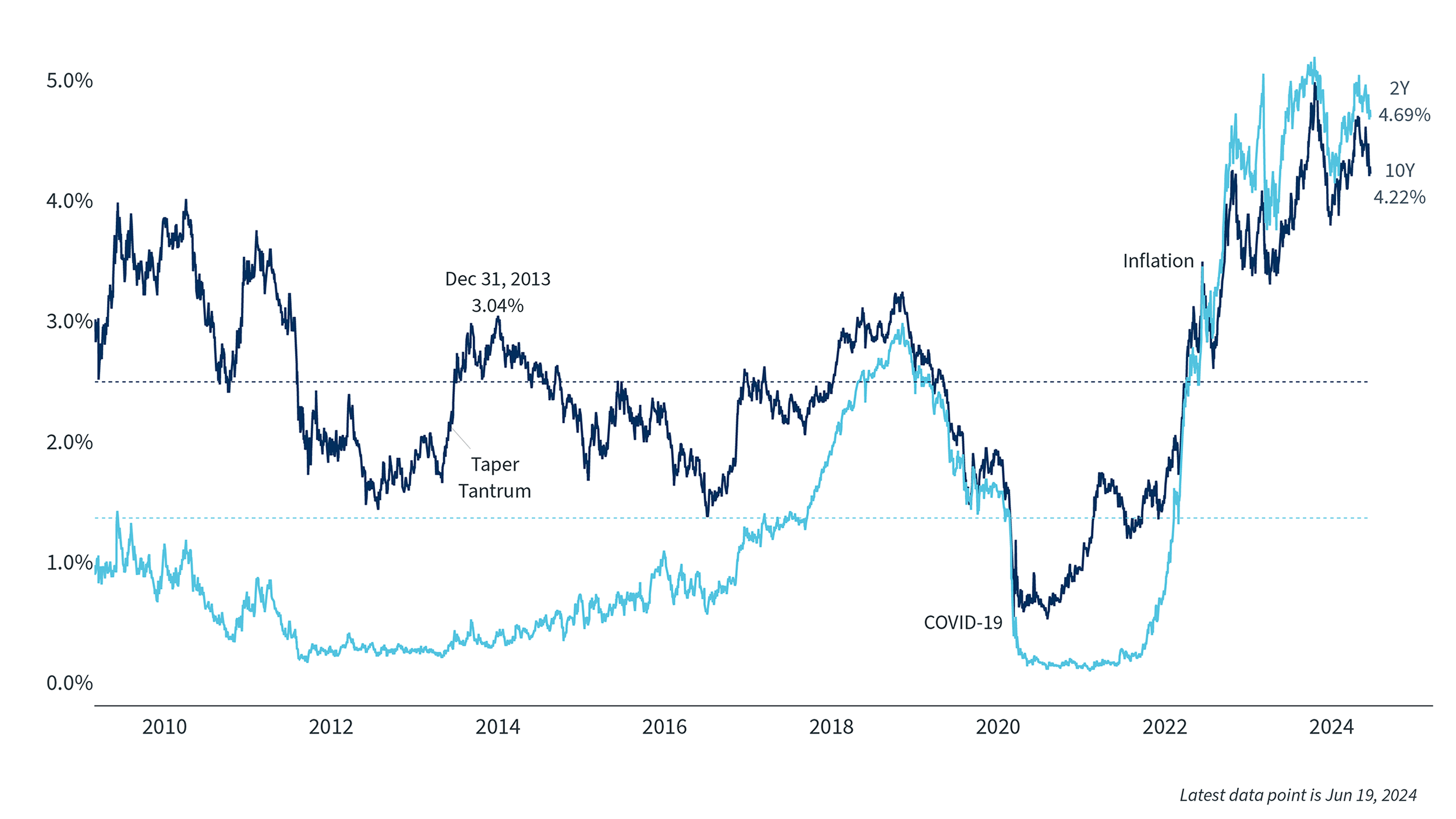

Looking forward, interest rates are still higher than many had expected and many CRE portfolios will need to be managed carefully in the coming years. This is because many projects were underwritten at sub-4% rates, roughly half of what they are now. The Fed’s recent rate hike cycle over the past two years has significantly altered the finances of many CRE portfolios. Many industry deals typically target net operating income (NOI) that is 20% greater than the debt payment. However, many borrowers have loan periods shorter than their expected loan amortization and are expected to refinance in the coming years.

Refinancing at significantly higher interest rates can mean that many existing projects are no longer feasible. In response to this, many lenders have taken additional collateral, and borrowers are paying down principal earlier. This highlights the importance of working with banking partners who know your business well and can offer creative solutions to limit refinancing risk.

Ultimately, the CRE industry has avoided some of the worst-case scenarios that many had predicted just a year ago. Still, high costs and interest rates have been a drag on the industry over the past 12 months, but we are beginning to see steadying in the market. While each sector is unique, the overall strength of CRE could begin to stabilize if interest rates, labor availability and other factors improve.

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cpath%20class='cls-1'%20d='M63,35.91c.05,14.91-12.02,27.03-26.99,27.12-14.79.09-26.95-12.03-27.01-26.91-.06-15.01,11.91-27.11,26.87-27.16,14.95-.05,27.08,12,27.13,26.95ZM45.08,18.32c-2.37,0-4.6-.07-6.82.02-3.32.14-5.55,1.94-6.61,5-.51,1.46-.62,3.07-.75,4.63-.12,1.45-.03,2.91-.03,4.54h-6.14v6.98h6.16v16.82h7.5v-16.89c1.6,0,2.98.05,4.34-.03.4-.02,1.05-.36,1.11-.65.4-2.02.67-4.06,1.01-6.3h-6.51c0-1.55,0-2.92,0-4.29,0-2.53,1.12-3.72,3.67-3.83,1-.05,2,0,3.06,0v-5.97Z'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cpath%20class='cls-1'%20d='M63,36.15c-.07,14.97-12.18,26.99-27.11,26.89-14.9-.1-26.92-12.16-26.89-26.99.03-15.01,12.15-27.11,27.15-27.08,14.87.03,26.92,12.23,26.85,27.18ZM36.62,51c.03-.53.08-.98.08-1.42,0-3.11-.04-6.22.02-9.33.05-2.49,1.88-4.31,4.23-4.36,2.31-.05,3.92,1.63,4,4.27.06,1.88.02,3.77.02,5.66,0,1.72,0,3.43,0,5.17h6.01c0-5.04.18-9.98-.07-14.91-.16-3.17-3.26-5.57-6.55-5.78-2.85-.18-5.44.35-7.56,2.83-.08-1.07-.14-1.75-.19-2.46h-5.83v20.33h5.84ZM27.06,30.66h-5.99v20.32h5.99v-20.32ZM24.06,20.18c-2.03-.03-3.64,1.57-3.66,3.65-.02,2.14,1.45,3.73,3.52,3.78,2,.05,3.74-1.57,3.82-3.56.08-2.04-1.63-3.84-3.68-3.87Z'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cg%3e%3cpath%20class='cls-1'%20d='M35.95,9.01c14.89-.05,27.01,12,27.05,26.9.04,14.88-12.08,27.09-26.9,27.08-14.88,0-27.08-12.13-27.1-26.93-.02-14.85,12.08-27,26.95-27.05ZM36.02,18.76c-2.54,0-5.09-.01-7.63,0-5.58.03-9.63,4.08-9.65,9.64-.01,5.09-.02,10.18,0,15.27.02,5.3,3.98,9.46,9.28,9.57,5.34.11,10.69.11,16.03,0,5.31-.11,9.22-4.26,9.24-9.58.02-5.19.03-10.38,0-15.57-.04-5.2-4.12-9.25-9.33-9.31-2.65-.03-5.29,0-7.94,0Z'/%3e%3cpath%20class='cls-1'%20d='M50.22,36.02c0,2.54.02,5.09,0,7.63-.03,3.73-2.68,6.49-6.41,6.54-5.19.06-10.37.06-15.56,0-3.7-.04-6.42-2.81-6.45-6.52-.04-5.14-.04-10.27,0-15.41.03-3.64,2.72-6.38,6.36-6.42,5.24-.06,10.48-.06,15.71,0,3.67.04,6.31,2.75,6.35,6.41.03,2.59,0,5.19,0,7.78ZM36.1,26.6c-5.11-.05-9.38,4.12-9.43,9.2-.05,5.28,4.02,9.53,9.18,9.59,5.26.07,9.54-4.07,9.66-9.35.11-5.02-4.25-9.4-9.41-9.44ZM43.25,26.81c.02,1.05,1.05,2.03,2.08,1.99,1.07-.04,2.04-1.06,1.92-2.12-.12-1.15-.78-1.84-1.98-1.87-1.13-.03-2.05.89-2.02,1.99Z'/%3e%3cpath%20class='cls-1'%20d='M42.2,36.07c-.04,3.39-2.95,6.22-6.3,6.13-3.35-.09-6.06-2.89-6.05-6.23,0-3.28,2.86-6.13,6.15-6.14,3.36,0,6.24,2.89,6.2,6.24Z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

%20--%3e%3cg%3e%3cg%20id='Layer_1'%3e%3cg%3e%3cpath%20class='cls-1'%20d='M8.99,36.02c0-14.9,12.03-27.02,26.87-27.06,14.99-.03,27.2,12.17,27.15,27.13-.05,14.95-12.18,26.99-27.14,26.94-14.9-.05-26.87-12.08-26.87-27.02ZM36,48.01c4.01-.29,8.03-.5,12.03-.89,2.54-.25,3.77-1.45,4.16-3.94.75-4.76.75-9.54.02-14.3-.39-2.56-1.67-3.79-4.23-4.08-7.98-.91-15.96-.92-23.94,0-2.67.31-4.16,1.68-4.27,4.36-.18,4.57-.17,9.15,0,13.71.1,2.6,1.56,3.98,4.19,4.24,4,.4,8.01.6,12.04.89Z'/%3e%3cpath%20class='cls-1'%20d='M41.32,35.97c-2.91,1.7-5.64,3.29-8.55,4.98v-9.87c2.87,1.64,5.61,3.21,8.55,4.89Z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)