Based on available information provided by companies in each sector who reported their earnings, as of September 17, 2020, the market has had a strong 3rd quarter.

While we had a very strong July and August, the equity market in September is down about 4.5 percent as tech companies come off their recent highs. Through September 13, Large Cap companies outperformed and are up almost 4.8 percent YTD while Mid Cap and Small Cap companies are down 9.02 percent and 9.41 percent YTD respectively.

Growth sectors have been outperforming value sectors so far. For value sectors, energy is down 44 percent, financials are down 18 percent, utilities are down 7 percent and real estate is down almost 7 percent. On the other hand, growth sectors are doing well with infotech up 24 percent, consumer discretionary up 22 percent and communication services are up almost 10 percent.

COVID-19 has created several key winners that drove the overall index performance. Winners have been consumer goods companies, technology companies and retail companies with ecommerce platforms like Target, Walmart and Amazon. Other companies such as homebuilders like Home Depot have also done quite well, as have gaming companies. Conversely, sectors that are hurt by COVID-19 include those in travel, hospitality, and entertainment like sporting venues and restaurants. Their businesses have yet to recover.

While the S&P 500 index has gone up and is positive today, this is really based on a few large technology, discretionary and consumer goods companies. The S&P 500 is a market-cap weighted index, which means that when large companies get more revenue and earnings relative to their smaller counterparts, their prices go up and they have more market cap. However, looking at the equal weighted market index, the index is down significantly compared to last year.

Although earnings for the first quarter and second quarter were down 13 percent and 7 percent respectively, the second quarter earnings came in better than expected. This is the result of strong consumer spending due to the stimulus package.

Equity Market

The equity market has rebounded due to a number of reasons. For instance, the Federal Reserve stepped in aggressively to calm the credit markets, and the huge fiscal relief provided by the government helped boosted consumer spending. New and speculative investors have joined the market since the pandemic started and there have been newer ways to treat and understand the virus and its implications. The anticipation of a vaccine has also contributed to a more optimistic outlook in the equity market.

However, there are many concerns that remain, which will invariably affect the equity market moving forward. Some include severe job loss since the start of the pandemic and over 100,000 businesses have yet to reopen since the lockdown. Businesses may face structural changes as they learn to compete and adapt to a post-COVID era. Other concerns include the trade war between the United States and China as well as changes in consumer behavior.

Overall, there is a Wall Street and Main Street disconnect, which means that while assets have staged a recovery, the economy has not. On a positive note, money market and bank deposits are at historically high levels. This means that people could start to invest more in equities again. Finally, stocks have rallied on the assumption that earnings will eventually recover.

Fixed Income Market

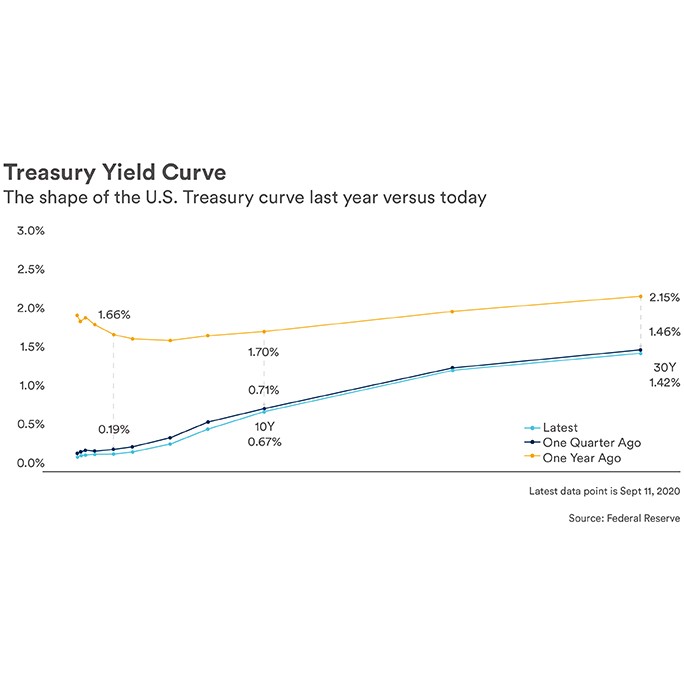

The treasury yield curve representing U.S. government bonds, which most fixed income sectors are benchmarked against, has stayed very flat. The treasury yield curve provides a good visual of where borrowing costs are with the two-year yield at 0.19 percent, the 10 yield at 0.67 percent, and the three yield being at 1.42 percent. The shorter yields are still at a record low around what they were in the 2008 and 2009 recession, with the long end of the curve reflecting expectations of low inflation and slow economic growth. Moving forward into the election and with continued uncertainty around the pandemic, there is an expectation of more volatility in the treasury market.

YTD performances across the board through the end of September 11:

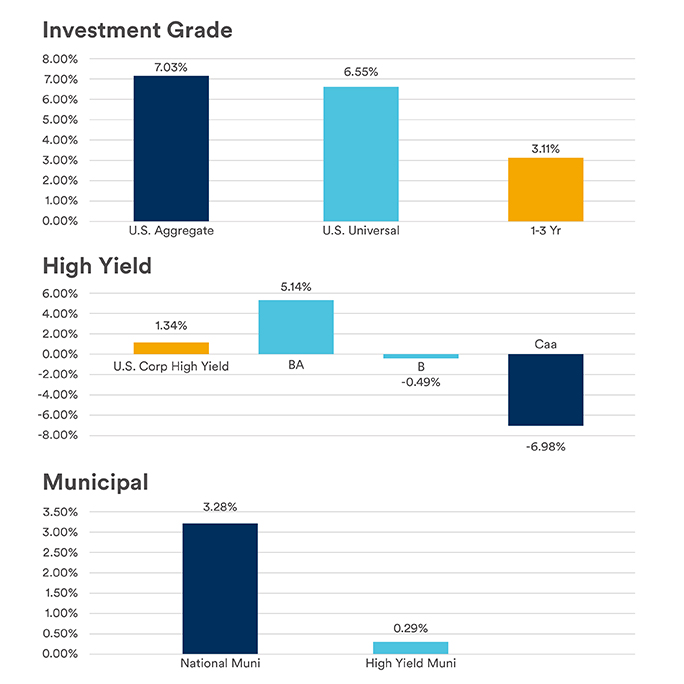

Investment grade space.

There’s been strong relative numbers across the higher quality investment grade space. U.S. aggregate space returned 7.03 percent, the U.S. universal space returned 6.55 percent, and the shorter one-to-three-year space returned 3.1 percent.

High yield space.

Not the best relative year-to-date performance. U.S. Corp high yield space returned 1.3 percent, Ba space returned 5.14 percent, B space was down 0.49 percent and Caa space was down 6.98 percent.

Municipal space.

Higher quality names have outperformed relative to the high yield muni. The national muni space returned 3.28 percent and the high yield muni returned 0.29 percent. However, with the effects of COVID-19, we can expect more volatility within the muni market.

Even though the high yield space has been hit hard on a YTD basis, federal support has caused these sectors to hold up relatively well, considering the economic environment we are currently in. And that is what continues to drive the fixed income market returns. There continues to be a large disconnect from the fundamentals because of the Fed's involvement, and this is likely to be the theme until the economy recovers from the pandemic.

In terms of federal rates, there appears to be consensus from the last federal meeting that there will not be a hike until 2023. The Fed is aiming for an inflation moderately above 2 percent for some time. So, we can expect an accommodative monetary policy until maximum employment and the average 2 percent inflation target is achieved. In addition, the Fed is committed to continuing its asset purchases through the Treasury – 80 billion a month in treasury securities and 40 billion a month in a mortgage backed securities agency. Overall, the Fed is making these commitments to sustain a functioning market, promote culminated financial conditions and support the flow of credit to households and business.

While there continue to be uncertainties surrounding the pandemic, our team is monitoring the economy closely with what Congress is doing and what the Fed is doing so as to take advantage of opportunities across all fixed income sectors when they arise.

Do note that the information provided is general in nature and based on our understanding of available information as of September 11, 2020. Please consult your financial advisor to discuss how the information presented here may impact your investments.